Björn Borg operates in the fashion industry and focuses on the design, manufacture and distribution of sportswear and underwear, accessories and bags. The company's products are aimed at men, women and children of all ages. The business is global with a main presence in the Nordic region and Europe. Björn Borg was founded in 1984 and has its headquarters in Solna.

In our view, Björn Borg has made good progress executing its strategy of expanding its core product categories and own e-commerce channel, which we expect to keep driving profitable growth.

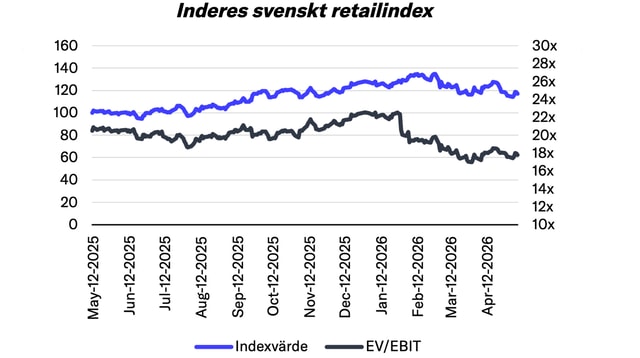

Årets första kvartal har varit utmanande för de noterade detaljhandelsbolagen. En orolig omvärld har satt press på konsumenten, som i hög grad bortprioriterat icke-nödvändiga inköp till förmån för det vardagliga. Dagligvaror och lågprisalternativ har tagit tydlig prioritet över investeringar i sällanköpsvaror som elektronik och varor till hemmet.

Björn Borg’s Q1 results came in above our expectations, and we view the share price reaction following the report as justified. While we have raised our short-term estimates following the Q1 beat, our mid- to long-term estimates remain largely unchanged. In our view, given the ongoing uncertainty in the operating environment and lack of clear evidence that the company can successfully scale its footwear segment, we believe the stock is already fairly priced for its expected earnings growth (2026e P/E: 17x). As a result, we reiterate our Reduce recommendation and target price of SEK 67 per share.

Björn Borg's Q1 revenue growth was better than our expectations, which in combination with increased gross margins resulted in a strong earnings beat. In our view, we view positivley on that sports apparel category contniues to show double-digit growth, however, there were yet no clear signs of an overall turnaround in the footwear category, which we belive will be key for the company to accelerate its revenue growth going forward.